State Auditor Challenges Arnold TDD as Millions in Taxes Continue to Be Collected

A newly released report from Scott Fitzpatrick, the State Auditor for Missouri, is raising serious questions about how the City of Arnold has managed millions of dollars collected through its Transportation Development Districts (TDD).

The audit, which examined years of activity tied to the Arnold Retail Corridor Transportation Development District (ARC TDD), outlines concerns ranging from improper use of funds to a lack of transparency with residents. In several instances, the report finds the district has operated outside the intended purpose of state law.

A System Built to Fund Transportation But Used Differently

Transportation Development Districts are designed to fund specific infrastructure projects, such as roads and intersections, through targeted sales taxes.

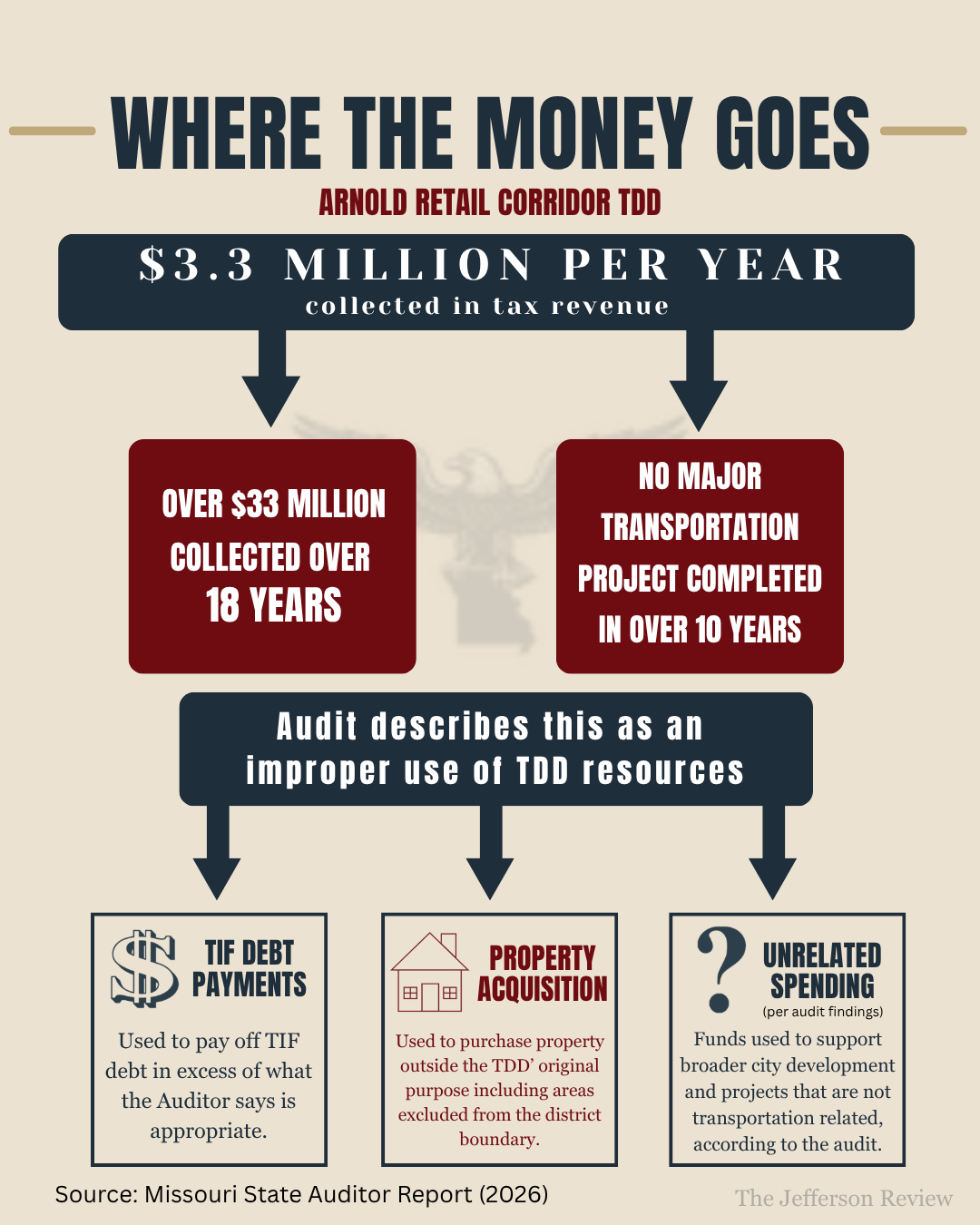

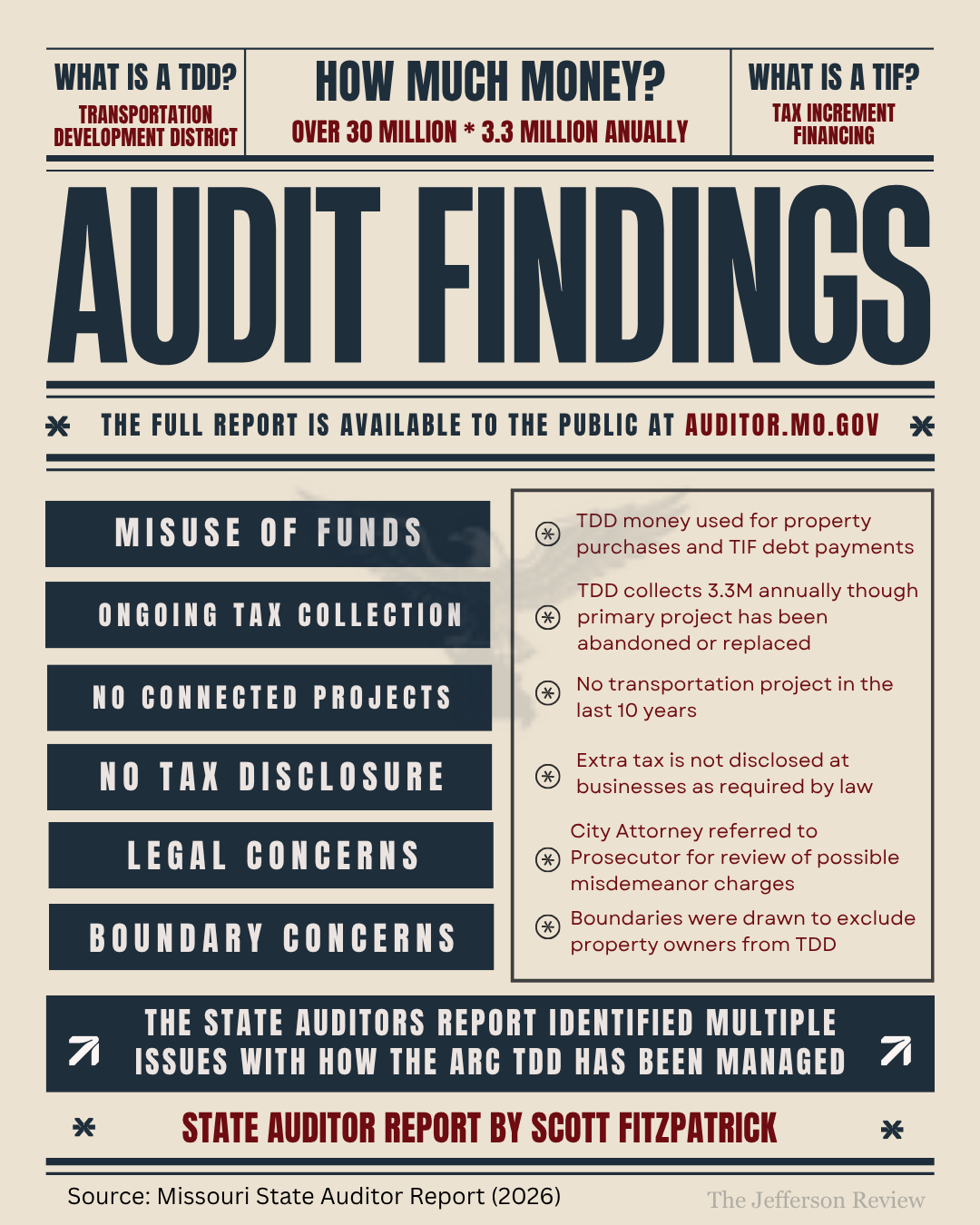

According to the audit, Arnold’s TDD has collected more than $33 million over its lifetime, including approximately $3.3 million annually in recent years. (see page 6 of the report)

However, Fitzpatrick says the district is no longer functioning in line with its intended purpose.

In an interview, Fitzpatrick was direct in his assessment:

“They haven't completed a transportation project in over a decade… they view this thing as a never-ending mechanism to tax the citizens of Arnold.”

The report also finds that the district has continued collecting taxes despite lacking a viable transportation project to justify its existence (see page 17 of the report ).

“Not Legitimate” Auditor Questions Foundation of the TDD

One of the most significant takeaways from the interview came when Fitzpatrick addressed the legitimacy of the district itself.

“The TDD is not legitimate in our view, and so it should be disbanded.”

He also noted that even if the district were considered valid, the amount of revenue being directed toward other obligations raises additional concerns.

“There is a limit to how much of that revenue should be used to pay off TIF debt… and they're going in excess of that.”

Where the Money Is Going

The audit outlines that TDD funds have been used in part to pay off Tax Increment Financing (TIF) debt tied to city development projects.

While some overlap between TDD and TIF funding is allowed under state law, the auditor found that Arnold exceeded what would be considered appropriate.

The audit concludes that TDD funds have been used for purposes unrelated to transportation, including development efforts and property acquisition. The report describes this as an “improper use of TDD resources” (see page 17 ).

Additionally, the audit found the city failed to file required TIF reporting documents in recent years, limiting transparency for both the City Council and the public (see page 37 ).

“They're collecting over three million… almost four million dollars a year… and most people probably aren’t even aware they’re paying this tax.”

The report further notes that businesses within the district were not properly displaying the additional tax, as required by law.

A Project That Has Shifted Over Time

At the center of the controversy is a long-discussed infrastructure effort, often referred to as the Arnold Parkway project.

While the city has publicly stated that the project is no longer moving forward, both the audit and statements from the State Auditor suggest that a related “connector road” project continues to be used as justification for ongoing tax collection. In practice, the projects appear closely tied, raising questions about whether the original effort has simply evolved or been reframed under a different name.

“They've tried to mislead the citizens… telling them we're not going to do this, and at the same time using that project as justification.”

The audit also notes that completing the connector road would require acquiring property outside the district boundaries. Concerns have been raised about how those boundaries were originally drawn and how decisions were communicated to the public. (see page 8)

City Attorney Named in Audit, Matter Referred

The report also includes a section addressing the actions of Arnold City Attorney Bob Sweeney.

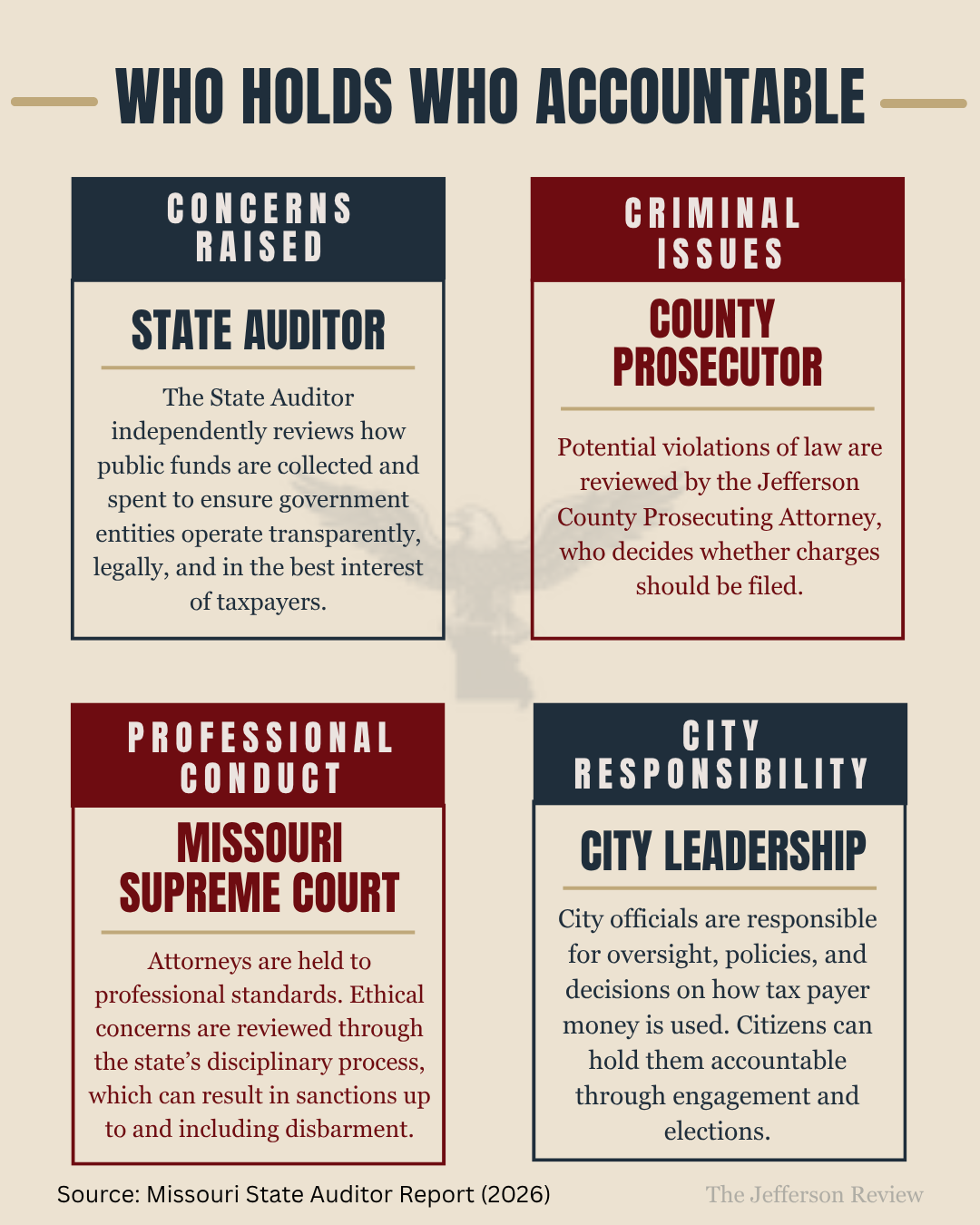

According to the auditor, Sweeney misrepresented his role during a meeting with auditors, indicating he served as legal counsel for the TDD when he did not. (see page 41). Fitzpatrick described this as a misdemeanor and referred his findings to the Jefferson County Prosecuting Attorney, Trisha Stefanski for review

“He was able to remain present… by virtue of misleading the auditors… which is a misdemeanor.”

Fitzpatrick confirmed that, as required by law, the matter was referred to the Prosecuting Attorney, whose office will determine whether any further action is warranted.

At the time of publication, the Jefferson Review reached out to the Jefferson County Prosecutor for comment, but was unable to obtain a response.

A Pattern Beyond One Issue

While some findings in the report point to potential legal violations, others fall into a different category.

“There were some areas where maybe there weren’t violations of the law, but the law was not used as it was intended.”

The auditor specifically pointed to how district boundaries were drawn to exclude affected residents from having a say in its creation. The report also raises concerns about how decisions were made and communicated, including limited public visibility into key aspects of the project.

What Happens Next

Fitzpatrick noted that the City of Arnold’s response to the audit stands out compared to other municipalities his office has reviewed.

“This is by far the least cooperative entity we've ever dealt with.”

While the State Auditor’s Office is responsible for identifying issues and, when necessary, referring matters for further review, enforcement now falls to other entities, including local prosecutors and state oversight bodies.

At the same time, the report places responsibility on local leadership to respond to its findings. City councils play a key role in how Transportation Development Districts are created and managed. While a TDD may operate as a separate entity, its leadership and direction are often closely connected to city officials. That means oversight and accountability ultimately fall to elected representatives

Advice to Residents From the Auditor

For residents trying to understand what this means for them, Fitzpatrick offered a direct message.

“You've been being overtaxed for a long time.”

He also pointed to recent changes in city leadership, noting the outcome of the most recent election.

“Every incumbent that was on the ballot for city council lost their election. My view is that citizens should make sure everyone now serving on the council is aware of what’s happening and that they’re not going to tolerate the city continuing to tax them in a way that’s not transparent and is funding activities it’s not supposed to fund.”

Fitzpatrick encouraged residents to remain engaged and hold local officials accountable. Residents who have concerns can attend council meetings, ask questions, and request clear explanations about how funds are being used. In situations like this, meaningful change often occurs at the local level. The findings are now public, the path forward will depend on how city leaders respond, and whether residents choose to engage.

If this report matters to you, don’t wait for someone else to explain what is happening in Jefferson County.

The Jefferson Review delivers local reporting, public meeting coverage, and the stories shaping your community directly to your inbox.

Stay informed. Stay involved. Subscribe free below.